Setting up your new committee as signatories at the bank should be a straightforward process, but it is often hampered by conflicting advice from staff within the same branch or different practices between branches. This leads to frustrated volunteers and can hold up running your P&C. Committees have also told us about practical difficulties with using electronic banking with ‘two to sign’ at some banks.

Setting up your new committee as signatories at the bank should be a straightforward process, but it is often hampered by conflicting advice from staff within the same branch or different practices between branches. This leads to frustrated volunteers and can hold up running your P&C. Committees have also told us about practical difficulties with using electronic banking with ‘two to sign’ at some banks.

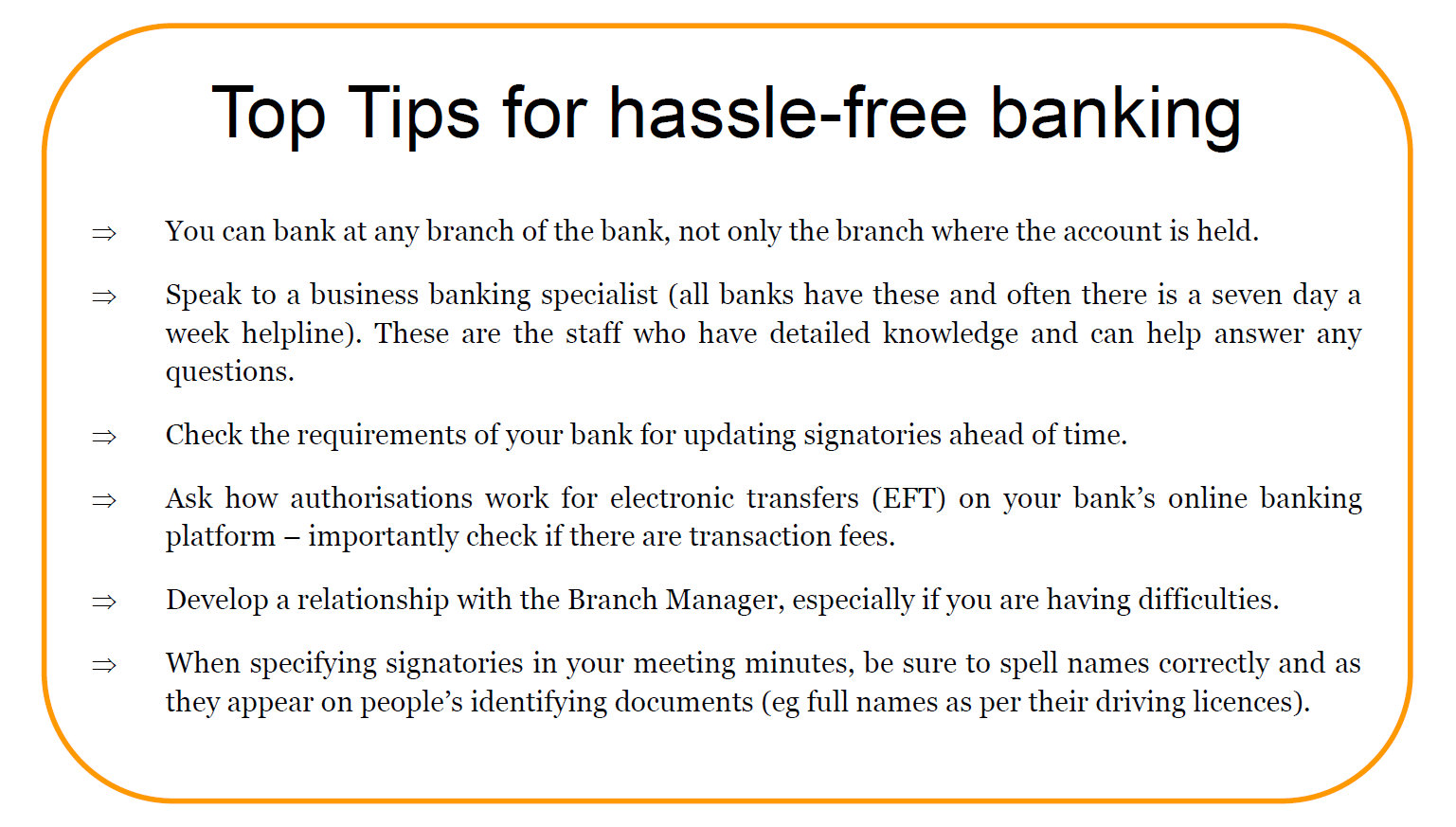

We spoke to the major banks to get a clearer picture for our members. We asked them which accounts are recommended for associations, how to update authorised account signatories, and how practical their ‘two to sign’ authorisation processes are for electronic transfers.

Banks: See what other P&Cs recommend - join the discussions on the Canberra P&C Leader's Facebook GroupLeader's Facebook Group.

Accounts for incorporated associations

Most banks have specific accounts for Incorporated Associations. Mostly these come under the umbrella of ‘Business Accounts’ and will often have the words ‘community’, ’non-profit’ or ‘society’ in their names. Examples include Bendigo Bank’s ‘Not for profit everyday account’, Westpac’s ‘Community Solutions One’ and Commonwealth and St. George Banks’ ‘Society Cheque Account’. Features of these types of accounts typically include no account keeping or transaction fees, a cheque book facility, and access to internet banking.

Opening a new account for an incorporated association usually requires:

- copy of your association’s constitution

- meeting minutes including the name of the association and naming the office bearers approved to open and operate the account

- Certificate of Incorporation (eg. St. George).

The president will need to be present and sometimes one other office bearer. All signatories should attend a branch to be identified and for a profile to be created on the bank’s systems if they are not an existing customer.

Updating Signatories

The banks we spoke to vary in their processes for updating signatories. So before organising your committee for a trip to the bank its best to check the requirements ahead of time. The bank’s business banking specialist will often be the best person to speak with to make sure you have the necessary documentation.

Banks such as Beyond Bank, ANZ and Commonwealth Bank, will provide a ‘signatory authority form’. Once filled in by all signatories each person can then visit the bank separately to have their identification verified and have a profile added. Other banks, like NAB, require all new and existing signatories to appear in person at the same time to be added and removed from the account. Beyond Bank also requires the signatures of signatories being removed although this can be done on a form with no need for the person at appear at the bank.

When updating your account signatories all banks require a copy of the minutes which detail the office bearers who are to be signatories to the account (for example a copy of the AGM minutes or any meeting where the signatories are agreed). It is best if the minutes specify which signatories will have access to internet banking and any other requirements specific to your account.

It is worth noting that if you need to make subsequent changes to the signatories, for example add a new signatory to the account, a new authorisation form may need to be filled in by all existing signatories and you will need to provide a copy of the minutes where the signatory updates have been agreed.

Two to sign options

Having online access to your account means you can check the balance at any time, print off statements and pay bills electronically (without the need to write cheques and wait for them to clear!). All the banks we spoke to allow internet banking by signatories and can give view-only or authorising access to committee members.

Most banks’ standard internet facility allows for two authorisers to complete transactions. The person initiating the payment will usually have to notify the co-signer that a transaction is ready to be authorised. The second person can then log in and authorise at a convenient time.

St. George and Westpac’s online banking allows for one or two signatories to act as administrators who can then set up access rights for the other signatories.

Commonwealth Bank electronic transfers require both signatories to be together at the one location, at the same time, to complete the transaction, which can be inconvenient for volunteers. ANZ’s ‘Internet Banking for Businesses’ offers a portable security device for two signatories. When a transaction is initiated, a security code is sent to each device and both codes are needed to complete the transaction. This means that both signatories don’t necessarily need to be together but do need to be able to communicate to relay the second code.

Other online business products are available such as ‘CommBiz’ and ‘NAB Connect’ which give extra functionality for your accounts and for authorising payments, as well as helping to manage payroll and interfacing with accounting software. However, these often come with transaction fees or other administrative costs, so you should consider whether these options suit the needs of your parent association. ●

For more on P&C Banking, see part 6 of the Treasurer's Handbook.

The advice in this article is general in nature and was correct at time of publishing (August 2019). P&Cs should seek professional advice and exercise judgement on banking products and services which are right for their individual circumstances.

This article appeared in ParentACTion Magazine, Term 3, 2019.